Best Savings Vehicles to Minimize College Debt

As of May 2025, over 43 million Americans carry federal student loan debt totaling $1.693 trillion! The average borrower owes more than $37,000 and 1 in 5 borrowers are behind on payments. These financial burdens often delay major milestones and other life goals.

The average family covers just 27% of college costs through scholarships and grants—leaving the rest to be paid out-of-pocket or borrowed. Despite the availability of college savings vehicles, student loans and parent income remain major sources of funding.

Choosing the right tools to save for your child’s education doesn’t have to be overwhelming. From tax-advantages to investment flexibility, each college savings account type has unique pros and cons. By understanding your options, you can make informed decisions that best suit your family’s goals.

In this blog, we break down the most popular college savings vehicles— to help you determine the best fit for your financial situation.

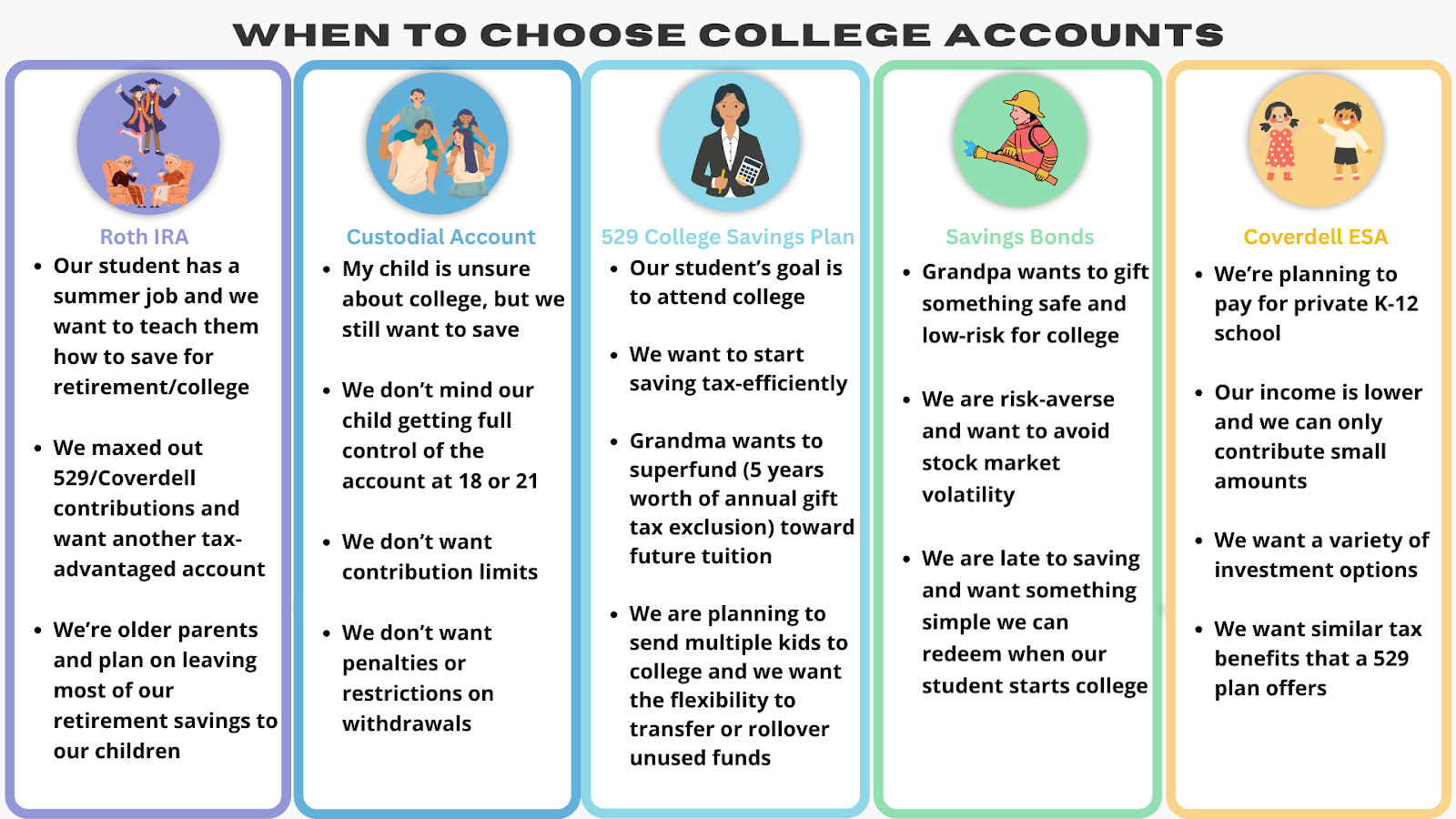

529 College Savings Plan

Best for: Parents with a long time horizon looking for a simple, tax-advantaged savings vehicle.

A 529 College Savings Plan is a state-sponsored investment account offering significant tax benefits for education expenses. These plans are the most popular way to save for college, due to their straightforward, tax advantaged structure. It is crucial to stay informed on 529 plan rules because there can be new changes every year that impact your strategy. For example, effective January 1, 2024, The SECURE 2.0 Act allows 529 tax-free and penalty-free rollovers to Roth IRAs.

Pros:

Tax-free growth and withdrawals for qualified education expenses like tuition, books, and room and board.

High contribution limits.

Minimal impact on financial aid. If 529 plans are owned by parents, 5.64% is calculated towards the Student Aid Index (SAI). If owned by grandparents it is 0%.

Potential state tax incentives, such as deductions or credits in some states (note: California does not offer this).

Ability to rollover $35,000 of unused or leftover funds to a Roth IRA (subject to conditions and lifetime limits).

Cons:

Non-qualified withdrawals will be subject to income tax and a 10% penalty.

Limited investment choices. You choose from a predefined set of portfolios, including age-based or target-date funds.

Qualified expenses for K-12 education are limited to only tuition (up to $10,000).

Coverdell ESA

Best for: Families seeking flexibility, tax-advantages, and planning for both K-12 and higher education costs.

A Coverdell ESA functions similarly to a 529 College Savings Plan by offering tax-free growth and withdrawals for qualified education expenses. Coverdell accounts have a wider range of qualified expenses, including many K-12 costs like tuition, books, supplies, tutoring, and uniforms, making them a versatile option.

Pros:

Tax-free growth and withdrawals for qualified educational expenses, for both K-12 and college.

Greater investment flexibility compared to 529 plans, allowing you to invest in individual stocks, mutual funds, ETFs, etc.

Cons:

Contribution limit of $2,000 per year per beneficiary, which may not be enough for some families. Specifically, those who are planning to send their students to out-of-state or private colleges.

Income limits apply to contributors, so high earners may not qualify.

Age restrictions apply. Funds must be used by the time the beneficiary is age 30—funds must be either spent on education or transferred to another eligible beneficiary.

Custodial Account

Best for: Parents whose children are unsure about college, but still want a backup plan. This account is great for parents who want full control over investments and contributions.

Custodial accounts (Uniform Gift to Minors Act or Uniform Transfers to Minors Act) allow you to set up an account in your child’s name, with an adult acting as a custodian until the beneficiary is of majority age. While not education-specific, these accounts are an excellent option for those looking for more flexibility in how their money can be utilized.

Pros:

No contribution limits—you can contribute as much as you want. (Subject to gift tax)

Funds can be used for anything that benefits the child, not just education.

Wide investment selection, including stocks, bonds, mutual funds, and more.

Cons:

There can be an impact on financial aid. Custodial accounts are considered the child’s asset, which can significantly reduce financial aid eligibility.

No tax advantages for education-specific use—funds are taxed as the child’s income. This account can be subject to Kiddie Tax, if the account generates more than $2,700 income (in 2025).

Control of the account shifts to the child once they reach the age of majority (18 or 21, depending on the state), so this account is not ideal if you only want your child to be able to use these funds for education.

Custodial accounts are irrevocable, which means that gifts are permanent and cannot be taken back. If you’re concerned your child may not use the funds wisely, this may not be an ideal account.

Roth IRA

Best for: Parents looking for an additional account that can be used for both retirement and college expenses.

A Roth IRA is more widely known as a tax-advantaged retirement account, offering tax-free growth and withdrawals in retirement. It was created to incentivize saving money for retirement but can also be used for qualified college expenses.

Pros:

Tax-free withdrawals of contributions (basis) at any time. You can always take out what you put in, but not the earnings. Early withdrawals of earnings will be subject to taxes and penalties.

Earnings can be withdrawn tax-free if used for qualified education expenses, as long as the account has been open for at least 5 years.

No negative impact on financial aid while the money remains in the child’s retirement account. Retirement accounts are not used in SAI (Student Aid Index).

Cons:

Contribution limits ($7,000 per year for 2025).

Withdrawals reduce retirement savings, which should generally be parents’ top financial priority–you generally want to avoid depleting retirement accounts early. The biggest advantage of a Roth is that your money is compounding and growing tax-free.

Earnings withdrawn from your Roth IRA impacts FAFSA Student Aid Index calculations, potentially reducing financial aid.

If you withdraw earnings prior to age 59.5, for reasons other than qualified expenses, a 10% penalty and income taxes apply.

Roth IRA contributions for your child, must use earned income from the child (W-2 income from a job, self-employment income, or employment in a parent’s business).

U.S. Savings Bonds

Best for: Conservative savers looking for safety, stability, and secure returns.

U.S. Savings Bonds are low-risk government bonds that can be used for qualified education expenses with some tax advantages. Interest earned may be tax-free if certain conditions are met.

Pros:

They provide principal protection and they are backed by the full faith and credit of the U.S. government.

There are tax advantages. Interest may be tax-free if used for qualified education expenses.

Cons:

Lower returns compared to equities.

Income limits apply for full tax-exemption on interest.

There are certain restrictions. Funds only apply to higher education tuition and fees and must be in the parent’s name to qualify for education tax exclusion.

Next Steps for Parents

Step 1: Set a savings goal for college and create a budget that allows you to achieve it.

Step 2: Assess your financial goals and priorities—determine whether you want complete control of funds or if you are fine with restrictions

Step 3: Review your state’s 529 plan options and note any state-specific benefits that may apply to you, especially if your state offers tax deductions or credits for contributions.

Step 4: Check the income limits for Coverdell ESAs and see if your income qualifies.

Step 5: Consult with a financial advisor to design a strategy that balances tax efficiency, investment growth, and your family’s long-term needs.

Step 6: Discuss your risk tolerance and preferred asset allocation with your advisor to ensure your investments align with your timeline and goals.

Step 7: Stay informed. Legislative changes and federal policy updates can affect your education savings plans.

How to Plan For Costs With Your Student

Don’t let college dictate your spending limits—that is one of the fastest ways to take on unnecessary debt. Instead, determine what your family can afford and choose schools that fit within that budget. Avoid creating a plan that relies on specific outcomes, like scholarships or financial aid, and hoping your finances will align later.

Empower your students. Avoid statements like, “We can only afford these colleges so you cannot go anywhere else.” Instead, tell them, “We want to help you find the best opportunities available and not graduate with debt or financial burden.” Positively framing the conversation matters.

Take this as an opportunity to teach your child about the value of money, trade offs, and long-term planning. Explain how college costs can affect other future goals—such as buying a home, planning a wedding, or even their own retirement. Managing finances is important before college, but it is even more crucial during and after.

It’s easy to get swept up in the social competition involved in the college admissions process. Remember, impressing your friends usually isn’t worth taking on excess debt that can ultimately derail your other goals. Keep in mind that college is just one piece of your overall financial pie.

Final Thoughts

Saving for college doesn’t have to be a complicated or a stressful experience. Start planning early and maximize your resources. Your goals and timeline are going to change, so flexibility and adaptability matters. Outcomes will always be different–college planning is never a one time event.

Do you want more information on college planning? Check out our blog, “Top 5 Mistakes Parents Make When Planning For College.”